The Telecom Regulatory Authority of India has recently issued a Consultation Paper on the Differential pricing for Data Services. This paper, and the final decision of TRAI on the same is likely to have a big impact on India, and on the world too, as the action taken by India would set the tone for similar action by developing countries world wide.

Much has been said about the issue of Net Neutrality. The FCC ruling on "Protecting and Promoting the Open Internet" of 12 March 2015 addresses the core issue in a comprehensive manner. The FCC identified the following Clear, Bright-Line Rules:

1. No Blocking: A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not block lawful content, applications, services, or non-harmful

devices, subject to reasonable network management.

2. No Throttling: A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not impair or degrade lawful Internet traffic on the basis of Internet content, application, or service, or use of a non-harmful device, subject to reasonable network

management.

3. No Paid Prioritization: A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not engage in paid prioritization. “Paid prioritization” refers to the management of a broadband provider’s network to directly or indirectly favor some traffic over other traffic, including through use of techniques such as traffic shaping, prioritization, resource reservation, or other forms of preferential traffic management, either (a) in exchange for consideration (monetary or otherwise) from a third party, or (b) to benefit an affiliated entity.

These are sound principles that the TRAI must consider adopting.

However, the current raging issue of "Free-Basics" is not in direct violation of the FCC ruling. Free basics is a form of paid prioritization through zero-rating. FCC notes in para 153 of its report "Given the unresolved debate concerning the benefits and drawbacks of data allowances and usage-based pricing plans, we decline to make blanket findings about these"

The FCC has also stated on the issue of Paid prioritization that: "The Commission may waive the ban on paid prioritization only if the petitioner demonstrates that the practice would provide some significant public interest benefit and would not harm the open nature of the Internet"

The TRAI needs to go further than the FCC in favouring net neutrality.

A clear and firm no to free-basics would be a step in that direction.

Here's my response to the issues raised in the TRAI consultation paper:

Much has been said about the issue of Net Neutrality. The FCC ruling on "Protecting and Promoting the Open Internet" of 12 March 2015 addresses the core issue in a comprehensive manner. The FCC identified the following Clear, Bright-Line Rules:

1. No Blocking: A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not block lawful content, applications, services, or non-harmful

devices, subject to reasonable network management.

2. No Throttling: A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not impair or degrade lawful Internet traffic on the basis of Internet content, application, or service, or use of a non-harmful device, subject to reasonable network

management.

3. No Paid Prioritization: A person engaged in the provision of broadband Internet access service, insofar as such person is so engaged, shall not engage in paid prioritization. “Paid prioritization” refers to the management of a broadband provider’s network to directly or indirectly favor some traffic over other traffic, including through use of techniques such as traffic shaping, prioritization, resource reservation, or other forms of preferential traffic management, either (a) in exchange for consideration (monetary or otherwise) from a third party, or (b) to benefit an affiliated entity.

These are sound principles that the TRAI must consider adopting.

However, the current raging issue of "Free-Basics" is not in direct violation of the FCC ruling. Free basics is a form of paid prioritization through zero-rating. FCC notes in para 153 of its report "Given the unresolved debate concerning the benefits and drawbacks of data allowances and usage-based pricing plans, we decline to make blanket findings about these"

The FCC has also stated on the issue of Paid prioritization that: "The Commission may waive the ban on paid prioritization only if the petitioner demonstrates that the practice would provide some significant public interest benefit and would not harm the open nature of the Internet"

The TRAI needs to go further than the FCC in favouring net neutrality.

A clear and firm no to free-basics would be a step in that direction.

Here's my response to the issues raised in the TRAI consultation paper:

Question 1: Should the TSPs be

allowed to have differential pricing for data usage for accessing different

websites, applications or platforms?

Response Q1: No. TSPs should not be allowed to

have differential pricing for data usage for accessing different websites,

applications or platforms.

Question 2: If differential pricing

for data usage is permitted, what measures should be adopted to ensure that the

principles of non-discrimination, transparency, affordable internet access,

competition and market entry and innovation are addressed?

Response Q2: A firm stand should be taken to prohibit

any form of differential pricing in data usage which directly impacts access to

specific parts of Internet. The justification for this stance is the “thin

edge of the wedge” argument - once differential pricing (including

Zero-rating for some content) for data is permitted, the TSPs can exercise the

power that they technically have to become active Gatekeepers of the Internet.

They can hold both the consumers of Internet, and the content providers to

ransom – and in the long run lead to the shrinkage of Internet access, and

simultaneous increase in cost of access. The content providers will be willing

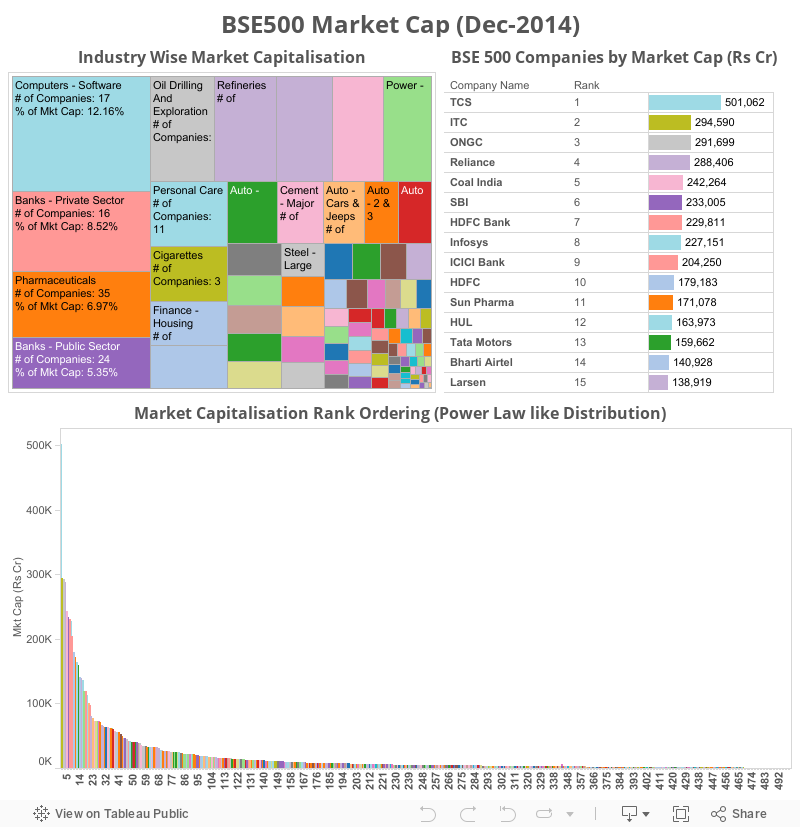

partners to this “ransom”. In a networked age where Power law distribution with

increasing concentration is becoming the norm, even a small advantage can make

all the difference between success and failure. Thus content providers would be

willing to pay a substantial amount to the TSPs to be given preferential

treatment in access to their site by consumers, say by getting it Zero-rated. If

this option of getting zero rated is kept open to all content providers without

any discrimination- then the advantage to any individual content providers is

lost, but the cost of content distribution

over the Internet would go up. This would adversely affect the dynamism and

innovation potential of Internet.

Question 3. Are there alternative

methods/technologies/business models, other than differentiated tariff plans,

available to achieve the objective of providing free internet access to the

consumers? If yes, please suggest/describe these methods/technologies/business

models. Also, describe the potential benefits and disadvantages associated with

such methods/technologies/business models?

Response Q3: Internet is all of the Web as we understand

it. Any subset of the Internet – say a few websites, and apps cannot be

called Internet. The zero-rated plans which allow access to a subset of Internet

cannot be construed as a model for providing universal access to Internet. They

are best viewed as sponsored content – and hence not at all meeting the “objective”

of providing free Internet access.

Enabling a certain basic access of Internet to all is a laudable objective.

Digital divide is understood to be a form of social and economic inequality

which needs to be tackled by society. However, since provisioning of Internet access

consumes economic resources, we need to accept that somebody has to pay for it

even if it is not the end consumer. The key decision lies in identifying the

party which would pay for Internet access to meet the societal goal of bridging

the digital divide.

One possible model of funding universal Internet access to meet the

challenge of Digital Divide is through the CSR spending which has been made mandatory

by the Companies Act 2013. The Act which

applies to large companies meeting certain financial criteria[1]

mandates such companies to spend a

minimum of 2 per cent of the average net profit made during the three

immediately preceding financial years. Government may make funding universal

internet access as one of the permissible activities for CSR spending, and

include it in Schedule VII of the Companies Act 2013.

All TSPs may then voluntarily contribute their CSR spend towards

providing this universal Internet Access.

The universal Internet access may be based on a bare bones data plan

to be specified by TRAI, comprising a fixed amount of data access (say 200 MB

per month to begin with – this can be periodically revised upwards). This plan can

then be made available by all TSPs to their subscribers for free – to the

extent of availability of funds. The plan may come with the rider that any

person who would like to consume Internet access more than the minimum provided

in the plan has to pay for additional access at a rate which also covers the

cost of the “free” component.

While it is understood that CSR contribution by the TSPs by themselves

would not be able to provide the basic Internet access to all their

subscribers, this can be supplemented by the CSR contributions from other

corporates. A suitable message can be displayed to the Internet consumer

informing him/her that the Internet access has been sponsored by the particular

corporate entity/TSP. TSPs may be encouraged to report on the number of

subscribers being provided free Internet access through such CSR funding.

Question-4: Is there any other issue

that should be considered in the present consultation on differential pricing

for data services?

Response Q4: TRAI may consider porting of Broadband

internet access service provider over mobile networks in the same way as

porting of mobile numbers ie unbundle Internet access from voice communication

service.

[1] Net

profit of Rs. 5 crore or more or net worth of Rs. 500 crore or more or a

turnover of Rs. 1000 crore or more in any financial year [Section 135(1)]